Ethylene Glycol Market Drivers: How Industry Changes Are Shaping the Future 2024 - 2031

Ethylene Glycol Market

Introduction

Ethylene glycol (C₂H₆O₂) is a colorless, odorless, and sweet-tasting organic compound primarily used as a raw material in the production of polyester fibers and polyethylene terephthalate (PET) resins. It also serves as a key ingredient in antifreeze formulations and industrial coolants due to its excellent heat transfer and anti-corrosive properties.

The global ethylene glycol market has experienced steady growth, driven by increasing demand from the automotive, textile, and packaging industries. Rapid urbanization, industrialization, and rising consumption of plastic products are major factors contributing to the expansion of the market. Additionally, the shift toward bio-based ethylene glycol, driven by environmental regulations and sustainability goals, is gradually reshaping the competitive landscape.

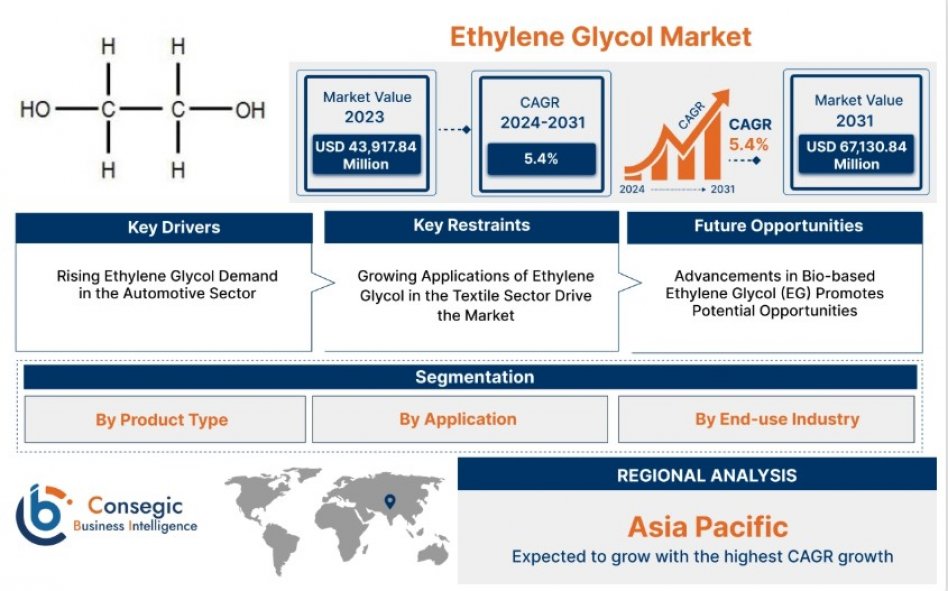

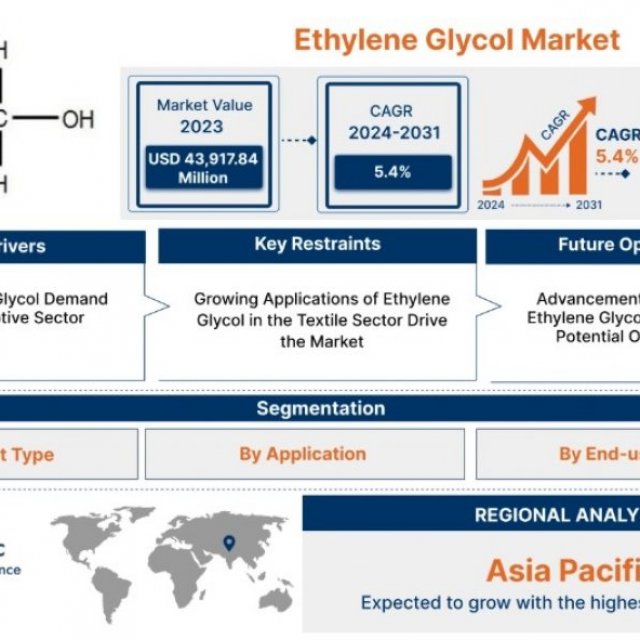

Ethylene Glycol Market Size

Ethylene Glycol Market size is estimated to reach over USD 67,130.84 Million by 2031 from a value of USD 43,917.84 Million in 2023 and is projected to grow by USD 45,527.86 Million in 2024, growing at a CAGR of 5.4% from 2024 to 2031.

Market Scope & Overview

The ethylene glycol market encompasses the production, distribution, and application of various types of ethylene glycol, including monoethylene glycol (MEG), diethylene glycol (DEG), and triethylene glycol (TEG). These are extensively used across industries such as automotive, textiles, packaging, and construction, mainly for manufacturing polyester fibers, PET resins, and as coolants or antifreeze agents. The market also includes the emerging segment of bio-based ethylene glycol, which is gaining traction due to environmental regulations and sustainability initiatives.

The market is global in nature, with Asia-Pacific leading in terms of consumption and production, followed by North America and Europe. Growth is fueled by increasing demand for synthetic fibers and plastic packaging, rising automotive production, and expanding infrastructure development. However, concerns over plastic waste, fluctuating crude oil prices, and regulatory pressures on petrochemical industries pose key challenges. Technological advancements and the adoption of eco-friendly alternatives are expected to shape the future trajectory of the market.

Ethylene Glycol Market Dynamics (DRO)

Drivers:

- Rising demand for polyester fibers and PET resins: With growing consumption in the textile and packaging industries, demand for monoethylene glycol (MEG), a key raw material, is increasing significantly.

- Expansion of the automotive industry: Ethylene glycol is widely used in antifreeze and coolant formulations, supporting market growth as global vehicle production increases.

- Rapid industrialization in emerging economies: Particularly in Asia-Pacific, increasing infrastructure development and manufacturing activities are boosting consumption of ethylene glycol-based products.

Restraints:

- Volatility in raw material prices: Ethylene glycol production depends heavily on ethylene, which is derived from crude oil and natural gas, making prices vulnerable to global energy market fluctuations.

- Environmental and health concerns: The non-biodegradable nature of some ethylene glycol-based products and their toxicity pose regulatory and public health challenges.

- Stringent environmental regulations: Government initiatives to curb plastic waste and promote sustainability are creating compliance pressures on manufacturers.

Opportunities:

- Shift toward bio-based ethylene glycol: Growing awareness of environmental sustainability is fueling innovation and investment in renewable, plant-based alternatives.

- Technological advancements in recycling and production: Improved recycling processes and catalysts for cleaner production methods present cost and efficiency benefits.

- Growth in electric vehicles (EVs): The increasing adoption of EVs is creating new demand for advanced coolant systems, where ethylene glycol plays a vital role.

Segmental Analysis of the Ethylene Glycol Market

By Product Type:

- Monoethylene Glycol (MEG): The most widely used type, primarily in polyester fiber and PET resin production. It dominates the market due to its extensive use in textiles and packaging.

- Diethylene Glycol (DEG): Used in the manufacture of unsaturated polyester resins, plasticizers, and as a solvent in paints, dyes, and oils.

- Triethylene Glycol (TEG): Commonly used in gas dehydration, as a solvent, and in air sanitizers and dehumidifiers.

By Application:

- Polyester Fiber & Resin Production: Major segment driven by demand in textiles, garments, and PET packaging.

- Antifreeze & Coolants: Used extensively in the automotive and industrial sectors for heat transfer and engine protection.

- Chemical Intermediates: For the synthesis of solvents, plasticizers, and other downstream chemicals.

- Others: Includes applications in deicing fluids, heat transfer fluids, and surfactants.

By End Use Industry:

- Textiles & Apparel: Largest consumer of MEG due to high polyester fiber demand.

- Automotive: Significant usage in antifreeze, coolants, and brake fluids.

- Packaging: Growing PET resin use in bottles and containers.

- Building & Construction: Applications in insulation and surface coatings.

- Oil & Gas: Use of TEG in natural gas dehydration.

- Others: Including pharmaceuticals, paints, and personal care.

By Region:

- Asia-Pacific: Dominates the market due to robust demand from China and India in textiles, packaging, and automotive sectors.

- North America: Mature market with consistent demand in automotive and industrial applications.

- Europe: Focused on sustainable and bio-based alternatives due to strict environmental regulations.

- Latin America: Emerging demand supported by economic development and rising industrial activity.

- Middle East & Africa: Growth driven by expansion in petrochemical and oil & gas sectors.

Top Key Players & Market Share Insights

The global ethylene glycol market is highly competitive and characterized by the presence of several major players with integrated operations across the value chain. Market share is concentrated among a few multinational corporations with strong regional footprints and production capacities.

- Akzo Nobel N.V. (Netherlands)

- Ashland (U.S.)

- China Petrochemical Corporation (China)

- Dow (U.S.)

- Formosa Plastics Group (Taiwan)

- Reliance Industries Limited (India)

- BASF (Germany)

- Huntsman International LLC (U.S.)

- INEOS (UK)

- LOTTE Chemical Corporation (South Korea)

- LyondellBasell Industries Holdings B.V. (UK)

Contact Us:

Consegic Business intelligence

Email : info@consegicbusinessintelligence.com

Sales : sales@consegicbusinessintelligence.com