Description

Clinical Data Management Systems (CDMS) Market

Introduction

The Clinical Data Management Systems (CDMS) market is a critical component of the modern clinical research and healthcare ecosystem, offering sophisticated software solutions designed to collect, manage, and analyze clinical trial data with accuracy and efficiency. As the pharmaceutical, biotechnology, and medical device industries face increasing pressure to accelerate time-to-market and comply with strict regulatory standards, the demand for robust and reliable data management platforms continues to rise.

Between 2023 and 2030, the CDMS market is expected to experience significant growth, driven by the surge in clinical trials, the adoption of electronic data capture (EDC) technologies, and the integration of artificial intelligence (AI) and machine learning (ML) in clinical workflows. Furthermore, the shift toward decentralized trials, growing emphasis on real-time data analytics, and the need for seamless integration with other eClinical systems are shaping the future of the industry.

Clinical Data Management Systems Market Size

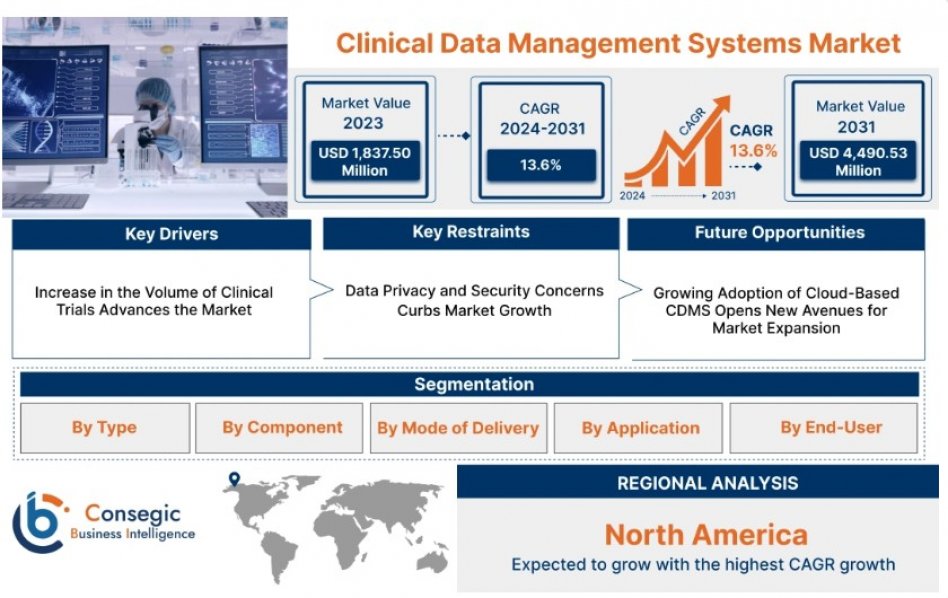

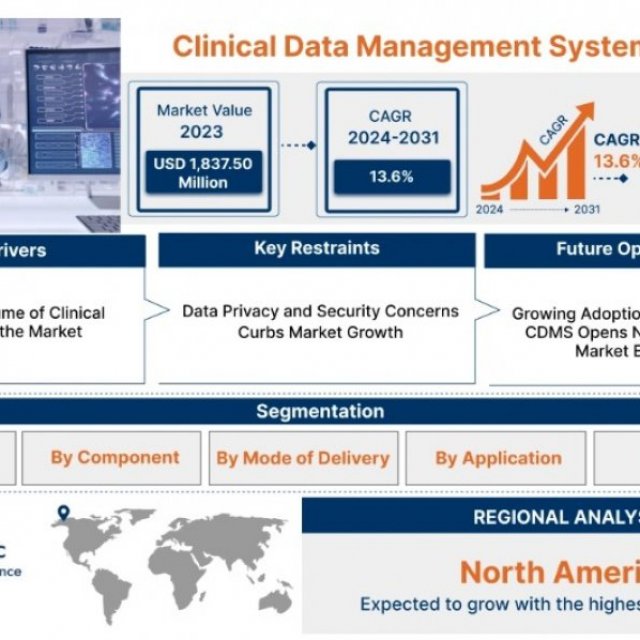

Clinical Data Management Systems Market size is growing with a CAGR of 13.6% during the forecast period (2024-2031), and the market is projected to be valued at USD 4,490.53 Million by 2031 from USD 1,837.50 Million in 2023.

Scope & Overview

The Clinical Data Management Systems (CDMS) market encompasses a wide range of software platforms and tools designed to streamline the collection, storage, validation, and analysis of clinical trial data. These systems are essential in ensuring data accuracy, regulatory compliance, and the overall integrity of clinical research processes. CDMS solutions are used extensively by pharmaceutical companies, contract research organizations (CROs), biotechnology firms, and academic institutions involved in clinical trials.

This report provides an in-depth analysis of the global CDMS market from 2023 to 2030, covering key market segments based on deployment models (on-premise, cloud-based), components (software, services), end-users (pharmaceutical companies, CROs, medical device companies, hospitals), and regions (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa).

Key areas of focus include:

The scope of this analysis also includes emerging opportunities, such as decentralized clinical trials (DCTs), wearable data integration, and regional expansions, offering stakeholders insights into both risks and rewards in the evolving CDMS market.

Market Dynamics (DRO)

The Clinical Data Management Systems (CDMS) market is shaped by a dynamic set of factors that influence its growth trajectory and adoption across the healthcare and life sciences sectors. Understanding these Drivers, Restraints, and Opportunities (DRO) is essential to grasp the market’s evolving landscape from 2023 to 2030.

Drivers

The increasing number of clinical trials across therapeutic areas, especially for chronic diseases, rare disorders, and emerging pandemics, is a key growth driver for CDMS platforms.

The shift from paper-based data collection to digital platforms has boosted efficiency, data accuracy, and regulatory compliance, fueling the demand for CDMS.

Growing emphasis on Good Clinical Practice (GCP), FDA 21 CFR Part 11, and GDPR is driving the need for secure, audit-ready, and standardized data systems.

Integration of AI, machine learning, and cloud-based solutions into CDMS platforms is enabling predictive analytics and real-time monitoring of trial data.

Restraints

The initial investment for advanced CDMS solutions, including software, integration, training, and maintenance, can be prohibitive for smaller organizations.

Handling sensitive patient data involves strict compliance with data protection laws. Any breach can have severe legal and reputational consequences.

Lack of trained personnel to manage, customize, and operate complex CDMS solutions can hinder adoption, especially in low-resource settings.

Opportunities

The growing adoption of virtual and hybrid trials has created opportunities for flexible, cloud-based CDMS that support remote data capture and monitoring.

Increased R&D investments, regulatory reforms, and growing clinical trial activity in Asia-Pacific, Latin America, and the Middle East open new growth avenues.

CDMS platforms that seamlessly integrate with EHRs, ePROs, CTMS, and wearable devices offer a comprehensive solution, enhancing market value and usability.

Segmental Analysis

By Type

By Component

By Mode of Delivery

By End-User

By Region

Top Key Players & Market Share Insights

The Clinical Data Management Systems market is highly competitive and dominated by several leading technology providers and contract research organizations. These companies are focusing on innovation, strategic partnerships, and global expansion to strengthen their market presence.

Contact Us:

Consegic Business intelligence

Email : info@consegicbusinessintelligence.com

Sales : sales@consegicbusinessintelligence.com

Reviews

To write a review, you must login first.

Similar Items

market research

market research

M3M3TIC

Digital Gyata